For credit unions, managing auto loan risk while continuing to support members can be challenging. When borrowers are unsure about insurance requirements or fail to maintain coverage, credit unions ma...

It’s been a tough year for millions of families. The coronavirus and subsequent social distancing measures put in place to help slow the spread of the disease caused major disruptions across nearly all industries in 2020. Although we have somewhat recovered from the initial shock of job losses in the spring, mass furloughs and layoffs have negatively affected millions of Americans—between February and August 2020, our nation lost nearly 11.6 million jobs. With government stimulus funds drying up and sluggish movement from Congress on further relief spending, this has created very real economic hardship for many families, which in turn is driving up delinquency rates.

When your collections team encounters a financially burdened borrower who genuinely wants to make his or her loan payments, but is going through a tough time financially, there are tactics your collections team can use to help them. In this blog post, we’ll discuss strategies for working with account holders hit hard by financial hardship.

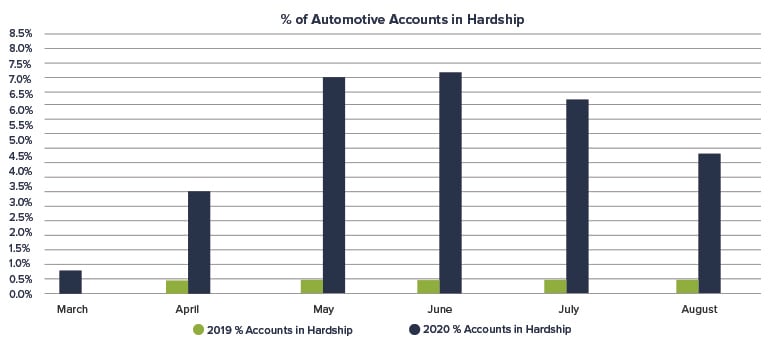

A Snapshot of Rising Economic Hardship in the Auto Lending Industry

Accounts in hardship are those that have been affected by a natural or declared disaster; reported as in forbearance; reported as deferred; or reported as having a frozen account status and/or past due notice. According to industry analysts at Black Book, “The number of accounts in hardship jumped substantially in April and kept increasing through June across all risk groups. The numbers stabilized in July and currently, about 4.3% of all accounts are in hardship, which is almost a 1,400% increase over last year. As deferrals expire in the upcoming month, coupled with a high unemployment rate, lenders expect a large portion of these hardships to become delinquencies.”

Empathy is Important

"I just lost my job and can't possibly pay you now," is a tough sentence to hear, and we all understand that, sometimes, life happens. Here are some empathetic responses that produce results:

-

Express that you're sorry to hear of the borrower's troubles; unfortunately, many others find themselves in this predicament.

-

Tell the borrower that since your institution understands this issue well, you work with borrowers to find a good compromise.

-

Depending on the outstanding balance, propose a reasonable amount for the borrower to pay today and a payment plan to pay off the rest.

-

Once you have an agreement on some payment today and a plan for the future, tell the borrower you will call again in 90 days to review the plan, with the hope that the borrower will be established in a new job by then.

Do Some Homework

Before a collector picks up the phone to speak to a borrower, they should do their homework. Having a complete picture of the borrower’s payment history will help assess risk, and provide insight about what's going on and how to approach the situation.

Related reading: The Top 8 Characteristics of Successful Collection Agents

Start by going through the notes associated with your borrower's account. Hopefully, your collections software can help paint an accurate story of your borrower and his or her payment history. You can also take your research one step further and run a soft pull of the borrower's credit report. When analyzing your borrower's notes and credit report, look for these six things that may indicate that they are in a financial predicament:

-

An increase in NSF activity

-

A significant change in credit score—particularly if it is decreasing

-

An increase in the number of unsecured credit accounts being opened

-

Escalating debt

-

An increase in delinquent accounts—especially accounts such as mortgages and auto loans

-

Changes in repayment habits—for example, making only minimum payments when they previously paid more

This high-risk activity, especially from a borrower who does not typically have delinquency issues, is a pretty good indication that they may be in financial trouble. If they are financially burdened you want to do everything you can, as quickly as possible, to work with them to find a viable solution that is mutually beneficial. After all, if they continue down the path of delinquency you both lose. So what can you do to help if all signs point to trouble for your borrower?

Build Rapport

Listen, truly listen, to your borrower’s situation to build the trust and rapport that is so essential to any successful relationship. When you talk to your borrower utilize effective interviewing techniques. Ask questions to help validate an accurate reflection of their current situation. Ask open-ended questions and stay away from questions that can be answered with ‘yes’ or ‘no.’ The key is to keep your borrower talking and give yourself an opportunity to listen carefully and observe clues that will help you determine the root cause of delinquency.

Find Common Ground

The best negotiators listen more than they talk, are respectful, and focus on finding common ground. You may ultimately want to be paid in full, however, use your best negotiation techniques to get some form of payment, even if it’s just a partial. Some payment is better than no payment, and your flexibility will go a long way with building that important rapport with your borrower.

While you're negotiating with your borrower, be sure to communicate the benefits of paying this debt over paying other financial obligations. What’s in it for them? Be prepared to communicate this benefit. In addition, be prepared to overcome inevitable objections. Most collectors can anticipate common objections, so be prepared and have your responses ready to go.

Arrive at a Mutually Beneficial Solution

When encountering a financially burdened borrower, strive to work with them to create a win-win solution for both parties. Communicate to your borrower that your goal is to find a mutually beneficial solution. You want to help them bring their account to a current status to avoid additional fees, charge-offs, or repossession. Look at each collection call as an opportunity to collaborate with your borrower to find a solution. This will help you build trust and strengthen the relationship the borrower has with your financial institution.

Incorporate Omnichannel Communication into Your Collections Efforts

Different demographics have different preferences when it comes to communicating and interacting with their lenders. As technology creates more contact options between you and your account holders, it’s important to keep pace with your borrowers’ preferences. Phone calls, emails, and text messages are all expected options for communication.

Consistency and redundancy across multiple channels is an important part of a broad communication strategy, as some borrowers will prefer one method while others may require multiple contact methods to gain top-of-mind awareness. Having regular communication touch points using multiple channels can help financially burdened borrowers access the information and resources they need to get out of arrears.

SWBC offers a scalable solution that saves our outsourced collections clients an average of 35-50% annually when compared to in-house efforts. Visit our website to see how much you could be saving today!

Let Us Know What You Thought about this Post.

Put your Comment Below.