Strait Ahead? Or are the Paths for Oil and Markets Still Erratic? The Strait of Hormuz has effectively reopened, with energy shipments once again moving through one of the world's most critical trade ...

Capital Markets

|

4 min read

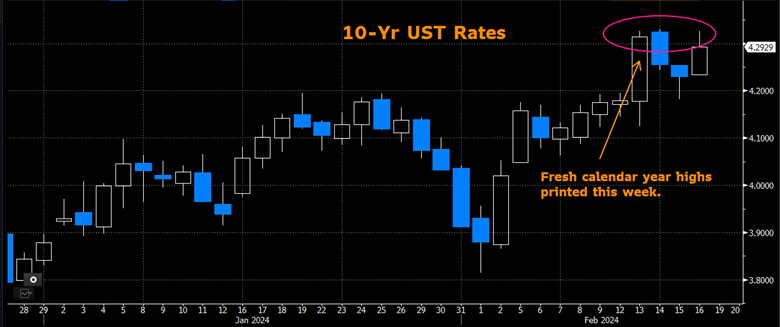

Right on cue, volatility returned to the markets last week after a relatively quiet period the week prior. Inflation concerns picked up again, with Consumer Price Index (CPI) prints coming in higher than expected on Tuesday, throwing cold water on the market’s inclination to lower rates. Notably, the strong support level in 10-year UST (4.19%) was taken out as rates closed at 4.33%. However, on Wednesday and Thursday, the market caught a bid and retraced much of this move but failed to recapture levels below 4.19% (now resistance). Friday, the strong Producer Prices Index (PPI) and the University of Michigan Consumer Sentiment data refueled the sell-off in rates, closing the week within the upper quintile of the weekly range.

The market has a near-term technical bias to test support levels, clearly putting 4.50% for 10-year UST in play. Investor sentiment suggested that the FOMC would cut rates in March, but this has abruptly changed. Talk that Powell & Co. may have to consider hiking rates has entered the conversation – to be fair, there is a low likelihood of this coming to fruition. That said, the virtual lock for a rate cut in March is off the table, with consensus settling on a cut at the June meeting. Keep in mind that the Fed has been very adamant about its concerns about cutting too quickly and having to reverse course. It was a herculean effort on the part of the policymakers to become comfortable with hitting the pause button, so drastic changes are not to be expected.

Municipals remained tight and well-bid despite last week's broader interest rate market experiencing shocks. The demand for paper remains robust, especially for specialty state credits and off-the-run names. The initial reaction to rates market volatility seems to result in a “pause” in the municipal market. Once the dust settles, however, buying resumes quickly, and sourcing new bonds are again challenges. We observed a strong market depth for more significant quality names, with most items receiving 15+ bids and tight covers.

Next week’s holiday-shortened session and a lighter economic data calendar set the stage for consolidation in both the rates and municipal markets. We expect many SWBC customers to look for value and opportunity to put some cash to work. Additionally, despite municipals remaining at less favorable ratios as a percentage of Treasuries, the more attractive absolute yields continue to draw buyers. During one recent discussion with a Portfolio Manager, she highlighted that the average investor in their SMA program does not think about their investments in the context of relative value versus Treasuries. If one can lock in attractive absolute yields on the customer's behalf, then the prudent course of action is to do so. Though it is early in 2024, with interest rates making a new high for the calendar year, putting some cash to work makes sense.

Definitions:

An index is unmanaged and not available for direct investment. Definitions sourced from Bloomberg.

The Bloomberg Barclays Global Aggregate Negative Yielding Debt Market Value Index represents the portion of the Bloomberg Barclays Global Aggregate Index that measures the aggregate value of global debt with a negative yield. • The S&P 500® is widely regarded as the best single gauge of large-cap U.S. equities and serves as the foundation for a wide range of investment products. The index includes 500 leading companies and captures approximately 80% coverage of available market capitalization. • The NASDAQ Composite Index is a broad-based capitalization-weighted index of stocks in all three NASDAQ tiers: Global Select, Global Market and Capital Market. The index was developed with a base level of 100 as of February 5, 1971.• The Cboe Volatility Index® (VIX) is a calculation designed to produce a measure of constant, 30-day expected volatility of the US stock market, derived from real-time, mid-quote prices of weekly S&P 500® Index (SPX) call and put options with a range of 23 to 37 days to expiration.• The ICE BofA MOVE Index is a yield curve weighted index of the normalized implied volatility on 1-month Treasury options. It is the weighted average of implied volatilities on the CT2 (Current 2 Year Government Note), CT5 (Current 5 Year Government Note), CT10 (Current 10 Year Government Note), and CT30 (Current 30 Year Government Note), with weights 0.2/0.2/0.4/0.2 respectively.• The Markit CDX North America Investment Grade Index is composed of 125 equally weighted credit default swaps on investment grade entities, distributed among 6 sub-indices: High Volatility, Consumer, Energy, Financial, Industrial, and Technology, Media & Tele-communications. Markit CDX indices roll every 6 months in March & September. • The Markit CDX North America High Yield Index is composed of 100 non-investment grade entities, distributed among 2 sub-indices: B, BB. All entities are domiciled in North America. Markit CDX indices roll every 6 months in March & September. • The U.S. Dollar Index (USDX) indicates the general international value of the USD. The USDX does this by averaging the exchange rates between the USD and major world currencies. Intercontinental Exchange (ICE) US computes this by using the rates supplied by some 500 banks.

Investing involves certain risks, including possible loss of principal. You should understand and carefully consider a strategy’s objectives, risks, fees, expenses, and other information before investing. The views expressed in this commentary are subject to change and are not intended to be a recommendation or investment advice. Such views do not take into account the individual financial circumstances or objectives of any investor that receives them. All indices are unmanaged and are not available for direct investment. Indices do not incur costs including the payment of transaction costs, fees, and other expenses. This information should not be considered a solicitation or an offer to provide any service in any jurisdiction where it would be unlawful to do so under the laws of that jurisdiction. Past performance is no guarantee of future results.

© 2021 SWBC. All rights reserved. Securities offered through SWBC Investment Services, LLC, a registered broker/dealer. Member FINRA & SIPC. Advisory services offered through SWBC Investment Company, a Registered Investment Advisor, registered as such with the US Securities & Exchange Commission. SWBC Investment Services, LLC is under separate ownership from any other named entity. SWBC Investment Services, LLC a division of SWBC, is a nationwide partnership of advisor.

Let Us Know What You Thought about this Post.

Put your Comment Below.