Strait Ahead? Or are the Paths for Oil and Markets Still Erratic? The Strait of Hormuz has effectively reopened, with energy shipments once again moving through one of the world's most critical trade ...

Capital Markets

|

4 min read

Everything seemed to be on cruise control last week, and for good reason. My kids were looking forward to a break from school; due to the Easter holiday and the ensuing spring break pause, they were happy to finish up their week on Thursday. In preparation for the holiday weekend, the markets remained relatively calm despite the release of the Fed's preferred inflation gauge on Friday, as the markets were closed. It is fair to suggest that the PCE Core Deflator came in largely as expected, with a 0.3% MoM reading and 2.8% YoY. However, the slight upward revision to January’s data from 0.4% to 0.5% MoM provides “just enough” reason to state that the Fed has no new incentive to change course. Chair Powell proclaimed, “We don’t need to be in a hurry to cut.” He added that the data is “… in line with what we want to see.”

The tragedy of the Francis Scott Key Bridge collapse in Baltimore adds a new challenge to the global economy, with supply chain issues making headlines again. Recalling the challenges caused by global supply chain disruptions due to COVID-19 lockdowns. Though clearly on a smaller scale, this disruption to the 9th largest US port threatens to reduce capacity, adding upward pressure to inflation. Furthermore, President Biden's plan to fund reconstruction adds an inflationary risk, as federal spending is typically inflationary.

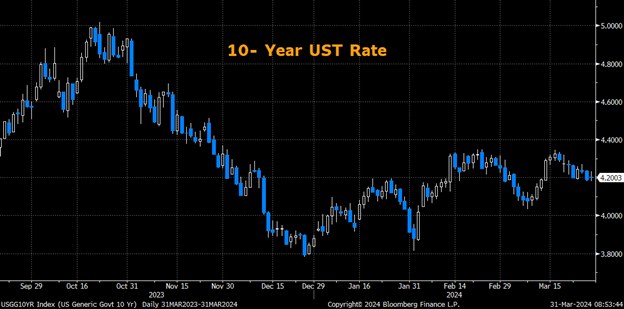

Rates drifted slightly lower during the week, but 10-year UST closed at 4.20%, remaining above recent resistance and within its recent range. Notably, municipals underperformed and increased along much of the curve despite the dip in Treasuries. Additionally, the front end of the municipal curve rose by 9-10 basis points in the 1 to 3-year range. This portion of the curve saw reduced participation among our clients, according to observations from the SWBC trading desk. As suggested in the past few commentaries, heading into the April 15th tax time, an overall slowdown in municipal buying activity amongst individual investors is expected. It is expected that the short-term section of the market will experience significant changes in activity. The employment data for March is likely to show that the labor market is stable. Any significant reaction from the market will only occur if there is an unexpected decline in the reading.

An index is unmanaged and not available for direct investment. Definitions sourced from Bloomberg.

The Bloomberg Barclays Global Aggregate Negative Yielding Debt Market Value Index represents the portion of the Bloomberg Barclays Global Aggregate Index that measures the aggregate value of global debt with a negative yield. • The S&P 500® is widely regarded as the best single gauge of large-cap U.S. equities and serves as the foundation for a wide range of investment products. The index includes 500 leading companies and captures approximately 80% coverage of available market capitalization. • The NASDAQ Composite Index is a broad-based capitalization-weighted index of stocks in all three NASDAQ tiers: Global Select, Global Market and Capital Market. The index was developed with a base level of 100 as of February 5, 1971.• The Cboe Volatility Index® (VIX) is a calculation designed to produce a measure of constant, 30-day expected volatility of the US stock market, derived from real-time, mid-quote prices of weekly S&P 500® Index (SPX) call and put options with a range of 23 to 37 days to expiration.• The ICE BofA MOVE Index is a yield curve weighted index of the normalized implied volatility on 1-month Treasury options. It is the weighted average of implied volatilities on the CT2 (Current 2 Year Government Note), CT5 (Current 5 Year Government Note), CT10 (Current 10 Year Government Note), and CT30 (Current 30 Year Government Note), with weights 0.2/0.2/0.4/0.2 respectively.• The Markit CDX North America Investment Grade Index is composed of 125 equally weighted credit default swaps on investment grade entities, distributed among 6 sub-indices: High Volatility, Consumer, Energy, Financial, Industrial, and Technology, Media & Tele-communications. Markit CDX indices roll every 6 months in March & September. • The Markit CDX North America High Yield Index is composed of 100 non-investment grade entities, distributed among 2 sub-indices: B, BB. All entities are domiciled in North America. Markit CDX indices roll every 6 months in March & September. • The U.S. Dollar Index (USDX) indicates the general international value of the USD. The USDX does this by averaging the exchange rates between the USD and major world currencies. Intercontinental Exchange (ICE) US computes this by using the rates supplied by some 500 banks.

Investing involves certain risks, including possible loss of principal. You should understand and carefully consider a strategy’s objectives, risks, fees, expenses, and other information before investing. The views expressed in this commentary are subject to change and are not intended to be a recommendation or investment advice. Such views do not take into account the individual financial circumstances or objectives of any investor that receives them. All indices are unmanaged and are not available for direct investment. Indices do not incur costs including the payment of transaction costs, fees, and other expenses. This information should not be considered a solicitation or an offer to provide any service in any jurisdiction where it would be unlawful to do so under the laws of that jurisdiction. Past performance is no guarantee of future results.

© 2021 SWBC. All rights reserved. Securities offered through SWBC Investment Services, LLC, a registered broker/dealer. Member FINRA & SIPC. Advisory services offered through SWBC Investment Company, a Registered Investment Advisor, registered as such with the US Securities & Exchange Commission. SWBC Investment Services, LLC is under separate ownership from any other named entity. SWBC Investment Services, LLC a division of SWBC, is a nationwide partnership of advisor.

Let Us Know What You Thought about this Post.

Put your Comment Below.